A parent of two college-age students, angry about the soaring cost of tuition, once asked me, “Everyone talks about student debt, but is there a debt bubble building among parents trying to help their kids pay for college?” The short answer may be yes. A recent Pew report, citing falling median net income and a generation of current and future parents saddled with unprecedented borrowing, warned of an “intergenerational legacy of debt” that will put extra pressure on college affordability.

It is widely reported that total student loan debt in the U.S. stands at about $1.2 trillion and has more than doubled in the past decade, rising much faster than inflation. Average student debt stands at about $30,000, but this masks considerable variation. Graduate students and those at for-profit schools tend to owe more, for example.

Still, student debt doesn’t tell the whole story. The casual observer might think that students pay for college solely through grants and federal loans. In reality, there is a big gap between the average annual net price of attendance (subtracting federal, state, and institutional grants and scholarships) and average annual loan debt. Students and families shoulder a considerable portion of the cost burden themselves.

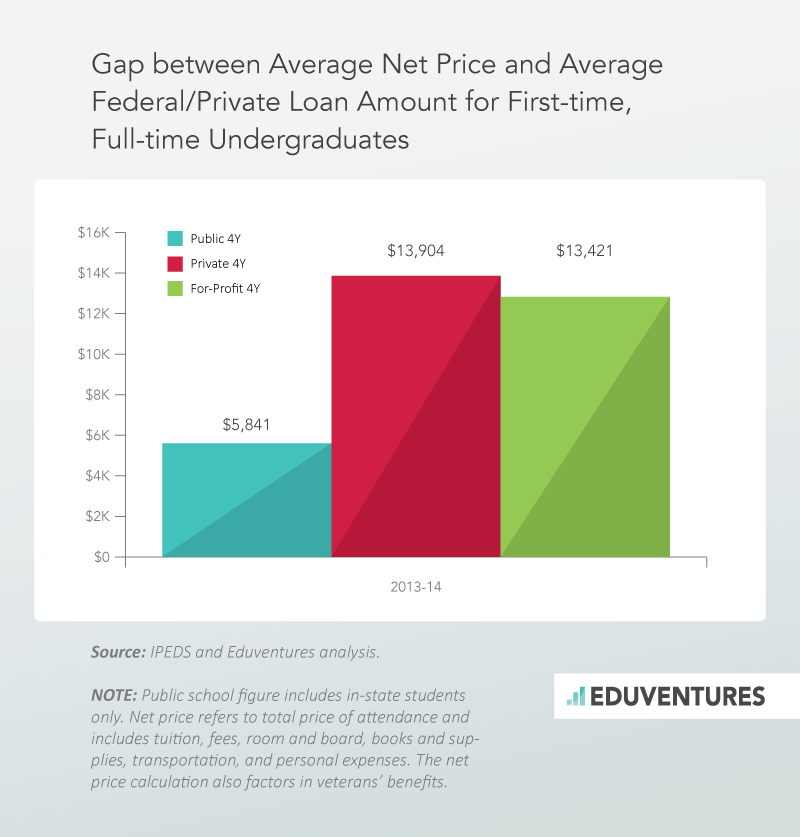

On average, federal and private loans cover only about 52% of net price at public 4-year schools. That’s an average annual funding gap of $5,800. At private and for-profit schools, the ratio is 35% and 39%, respectively, leaving students and families responsible for about $14,000 and $13,500 a year, on average. In recent years, relative funding gaps have been reasonably stable.

The fact that students and families pay about 50-65% of net tuition themselves is not news to anyone with a kid in college, but it tends to go unremarked in policy discussions and media coverage. Of course, these are averages, so some students and families pay a lot less out-of-pocket, and others pay more.

Is the fact that many students and families cover a major portion of tuition a sign of economic health or a hidden tax that further undermines the pretense of college affordability?

Where does the extra money come from?

Small contributions come from lots of sources, like Work-Study, private loans, PLUS loans for parents, and student credit cards. On average, these sources either impact fewer than 10% of students or contribute little to paying for college. In terms of employment, the majority of students earn less than $10,000 a year according to the National Postsecondary Student Aid Study (NPSAS). Fewer than 10% earn more than $15,000. For in-state students at public schools, a decent salary may cover out-of-pocket college expenses. At private and for-profit schools, few students earn enough to close the gap.

To return to my friend’s question, what about parents?

Debt statistics call out student loans but are silent on the proportion of other debt (e.g., credit cards and home equity) devoted to education expenses. In fact, there appears to be no data on the parental contribution, whether from income or loans, to the average college funding gap.

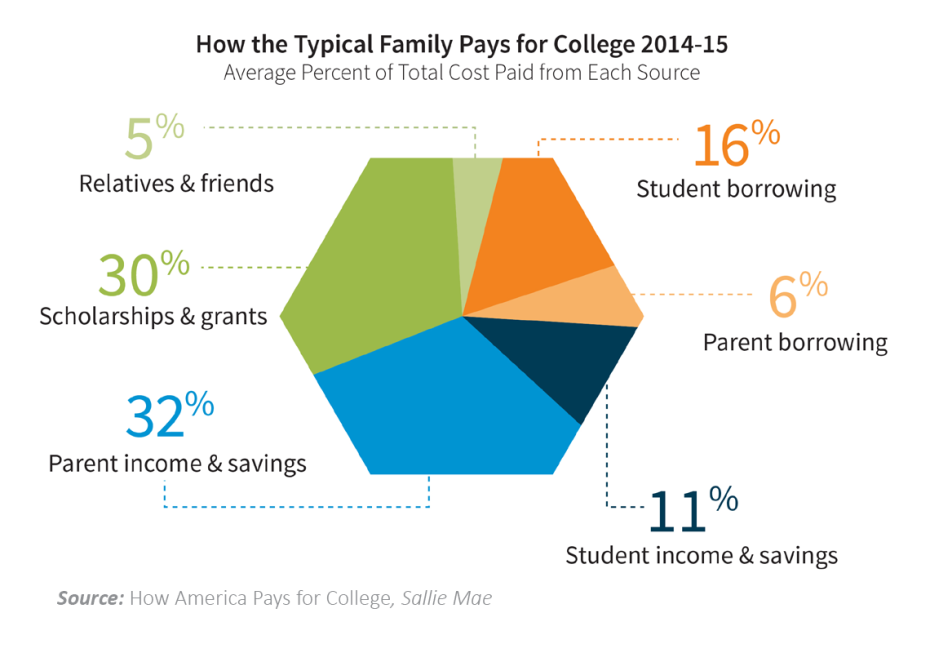

The best proxy is Sallie Mae’s annual How America Pays for College report, which is based on phone interviews with 1,600 parents and students nationally and examines the total cost of attendance, not the funding gaps after grants and loans. In 2014-15, parental income and savings supplied 32% of the total cost of attendance, and parent private borrowing only supplied 6%. Between these sources, parents contributed nearly 40% of total college costs. These ratios have been broadly stable since the survey was launched in 2008. Withdrawal from retirement funds accounts for less than 1% of college spending.

On average, federal and private loans cover only about 52% of net price at public 4-year schools. That’s an average annual funding gap of $5,800. At private and for-profit schools, the ratio is 35% and 39%, respectively, leaving students and families responsible for about $14,000 and $13,500 a year, on average. In recent years, relative funding gaps have been reasonably stable.

The fact that students and families pay about 50-65% of net tuition themselves is not news to anyone with a kid in college, but it tends to go unremarked in policy discussions and media coverage. Of course, these are averages, so some students and families pay a lot less out-of-pocket, and others pay more.

Is the fact that many students and families cover a major portion of tuition a sign of economic health or a hidden tax that further undermines the pretense of college affordability?

Where does the extra money come from?

Small contributions come from lots of sources, like Work-Study, private loans, PLUS loans for parents, and student credit cards. On average, these sources either impact fewer than 10% of students or contribute little to paying for college. In terms of employment, the majority of students earn less than $10,000 a year according to the National Postsecondary Student Aid Study (NPSAS). Fewer than 10% earn more than $15,000. For in-state students at public schools, a decent salary may cover out-of-pocket college expenses. At private and for-profit schools, few students earn enough to close the gap.

To return to my friend’s question, what about parents?

Debt statistics call out student loans but are silent on the proportion of other debt (e.g., credit cards and home equity) devoted to education expenses. In fact, there appears to be no data on the parental contribution, whether from income or loans, to the average college funding gap.

The best proxy is Sallie Mae’s annual How America Pays for College report, which is based on phone interviews with 1,600 parents and students nationally and examines the total cost of attendance, not the funding gaps after grants and loans. In 2014-15, parental income and savings supplied 32% of the total cost of attendance, and parent private borrowing only supplied 6%. Between these sources, parents contributed nearly 40% of total college costs. These ratios have been broadly stable since the survey was launched in 2008. Withdrawal from retirement funds accounts for less than 1% of college spending.

When it comes to paying for college, parent income and savings are much more important than parent borrowing, on average. Parents are crucial to making the college cost equation work but are primarily drawing on wealth, not debt. Everything looks manageable and stable, even if the parent who inspired this post is not very happy about the situation.

Looking to the future, the Pew report takes a more skeptical tone. The authors focus on Generation X graduates, who are much more likely to have student debt than previous generations. Gen Xers, those born between 1965 and 1980, with student debt are less likely to save for college for their own children and report saving a fifth as much as peers with no student debt ($4,000 vs. $20,000). This “intergenerational legacy of debt” may inhibit college access and increase to the prevalence of borrowing.

There are certainly reasons to worry. Over the past decade, median household income has not kept pace with inflation. Even if the net price of college tracks close to consumer costs, pressure on income will weaken affordability. Historical student debt will start to weigh on college decision-making as never before. Throw in pressure on retirement funds and inadequate saving by most adults, too. No wonder a number of presidential candidates are championing “free college.”

Ultimately, everything boils down to ROI. A degree continues to command a substantial wage premium, making debt a good investment for many. Higher education is vulnerable to the surge of interest, at least among edtech companies, in alternative credentials designed to increase value and lower cost. As always, schools will benefit by doing more to show why their degree offers a good return in every sense.

If income and debt trends continue, the quiet dependability of parents may become anything but.

Look out for forthcoming Eduventures research on how prospective students are factoring affordability into their decision-making and our Student Experience Dashboard, which is in its pilot phase and evaluates institutional value claims against peer benchmarks.

When it comes to paying for college, parent income and savings are much more important than parent borrowing, on average. Parents are crucial to making the college cost equation work but are primarily drawing on wealth, not debt. Everything looks manageable and stable, even if the parent who inspired this post is not very happy about the situation.

Looking to the future, the Pew report takes a more skeptical tone. The authors focus on Generation X graduates, who are much more likely to have student debt than previous generations. Gen Xers, those born between 1965 and 1980, with student debt are less likely to save for college for their own children and report saving a fifth as much as peers with no student debt ($4,000 vs. $20,000). This “intergenerational legacy of debt” may inhibit college access and increase to the prevalence of borrowing.

There are certainly reasons to worry. Over the past decade, median household income has not kept pace with inflation. Even if the net price of college tracks close to consumer costs, pressure on income will weaken affordability. Historical student debt will start to weigh on college decision-making as never before. Throw in pressure on retirement funds and inadequate saving by most adults, too. No wonder a number of presidential candidates are championing “free college.”

Ultimately, everything boils down to ROI. A degree continues to command a substantial wage premium, making debt a good investment for many. Higher education is vulnerable to the surge of interest, at least among edtech companies, in alternative credentials designed to increase value and lower cost. As always, schools will benefit by doing more to show why their degree offers a good return in every sense.

If income and debt trends continue, the quiet dependability of parents may become anything but.

Look out for forthcoming Eduventures research on how prospective students are factoring affordability into their decision-making and our Student Experience Dashboard, which is in its pilot phase and evaluates institutional value claims against peer benchmarks.

On average, federal and private loans cover only about 52% of net price at public 4-year schools. That’s an average annual funding gap of $5,800. At private and for-profit schools, the ratio is 35% and 39%, respectively, leaving students and families responsible for about $14,000 and $13,500 a year, on average. In recent years, relative funding gaps have been reasonably stable.

The fact that students and families pay about 50-65% of net tuition themselves is not news to anyone with a kid in college, but it tends to go unremarked in policy discussions and media coverage. Of course, these are averages, so some students and families pay a lot less out-of-pocket, and others pay more.

Is the fact that many students and families cover a major portion of tuition a sign of economic health or a hidden tax that further undermines the pretense of college affordability?

Where does the extra money come from?

Small contributions come from lots of sources, like Work-Study, private loans, PLUS loans for parents, and student credit cards. On average, these sources either impact fewer than 10% of students or contribute little to paying for college. In terms of employment, the majority of students earn less than $10,000 a year according to the National Postsecondary Student Aid Study (NPSAS). Fewer than 10% earn more than $15,000. For in-state students at public schools, a decent salary may cover out-of-pocket college expenses. At private and for-profit schools, few students earn enough to close the gap.

To return to my friend’s question, what about parents?

Debt statistics call out student loans but are silent on the proportion of other debt (e.g., credit cards and home equity) devoted to education expenses. In fact, there appears to be no data on the parental contribution, whether from income or loans, to the average college funding gap.

The best proxy is Sallie Mae’s annual How America Pays for College report, which is based on phone interviews with 1,600 parents and students nationally and examines the total cost of attendance, not the funding gaps after grants and loans. In 2014-15, parental income and savings supplied 32% of the total cost of attendance, and parent private borrowing only supplied 6%. Between these sources, parents contributed nearly 40% of total college costs. These ratios have been broadly stable since the survey was launched in 2008. Withdrawal from retirement funds accounts for less than 1% of college spending.

When it comes to paying for college, parent income and savings are much more important than parent borrowing, on average. Parents are crucial to making the college cost equation work but are primarily drawing on wealth, not debt. Everything looks manageable and stable, even if the parent who inspired this post is not very happy about the situation.

Looking to the future, the Pew report takes a more skeptical tone. The authors focus on Generation X graduates, who are much more likely to have student debt than previous generations. Gen Xers, those born between 1965 and 1980, with student debt are less likely to save for college for their own children and report saving a fifth as much as peers with no student debt ($4,000 vs. $20,000). This “intergenerational legacy of debt” may inhibit college access and increase to the prevalence of borrowing.

There are certainly reasons to worry. Over the past decade, median household income has not kept pace with inflation. Even if the net price of college tracks close to consumer costs, pressure on income will weaken affordability. Historical student debt will start to weigh on college decision-making as never before. Throw in pressure on retirement funds and inadequate saving by most adults, too. No wonder a number of presidential candidates are championing “free college.”

Ultimately, everything boils down to ROI. A degree continues to command a substantial wage premium, making debt a good investment for many. Higher education is vulnerable to the surge of interest, at least among edtech companies, in alternative credentials designed to increase value and lower cost. As always, schools will benefit by doing more to show why their degree offers a good return in every sense.

If income and debt trends continue, the quiet dependability of parents may become anything but.

Look out for forthcoming Eduventures research on how prospective students are factoring affordability into their decision-making and our Student Experience Dashboard, which is in its pilot phase and evaluates institutional value claims against peer benchmarks.

Thank you for reading our weekly Wake-Up Call. We’re offering our readers a free download of Part One of our Survey of Admitted Students, Balance Yield Activity: Recruiting Different Decision Segments.Click here to download the report.

Thank you for reading our weekly Wake-Up Call. We’re offering our readers a free download of Part One of our Survey of Admitted Students, Balance Yield Activity: Recruiting Different Decision Segments.Click here to download the report.