A Message from our CEO, Patrick Vogt: As we approach the end of the academic year, we recognize the increasing pressure that higher education leaders now face as they look towards the fall semester. Colleges and universities are struggling to navigate the difficult decisions that come with the reality of reopening campuses amid an ongoing global pandemic. Ensuring the safety of every student, faculty, and staff member remains the number one priority.

How do institutions implement social distancing on campuses designed for population density and collaboration to enhance the learning experience? These are difficult decisions, and we understand and respect the process. At ACT | NRCCUA, we are committed to being a trusted resource for all of our members by providing institutions with timely and relevant answers to the real-world questions that you are now facing in light of COVID-19. I want to assure you that our entire team is here to help you and your institution through this unprecedented crisis.

I hope you find this week's Wake-Up Call helpful. We have included an excerpt from our recent Insights report, Fall 2020 Enrollment Scenarios, Part 1: Traditional-Aged Undergraduates, available to members on Encoura Data Lab. For questions around access to Data Lab, please contact us.

As the weeks go by, higher education leaders face the looming prospect of a fall semester during a pandemic, amid the sharpest economic contraction in nearly a century. While we all hope the virus will retreat come fall and the economy will be on the rebound, sound planning means anticipating unwelcome scenarios. Some commentators expect, in tune with recent recessions, a fall enrollment surge, while others worry that this downturn will be so severe and peculiar that a rout is more likely.

Here, we weigh the variables on which fall 2020 will turn starting with traditional-aged, domestic undergraduates at four-year schools.

We Want College, Can You Give it to Us?

Unlike adult learners, who enroll in far greater numbers when the economy tanks, domestic traditional-aged undergraduate enrollment has been driven by population size, high school graduation rate gains, and a broadening view that a college education is increasingly essential for at least a middle-class lifestyle. In years past, we’ve seen little impact of recessions on this college-going population.

In the Great Recession of 2007-09, until now the worst GDP crunch since the Depression, traditional-aged undergraduate enrollment grew about 3% in fall 2007 and fall 2008. The downturn coincided with perhaps the largest high school graduating classes in U.S. history, boosting enrollment regardless.

From 2009 onward, the enrollment curve started to flatten for this population, as underlying size stabilized or started to fall, and high school graduation rates plateaued in many states. This trend continued up to 2019, although many four-year schools, particularly larger publics, have continued to grow enrollment.

Insofar as the COVID-19 recession looks to be much worse than the last one, even the traditional-aged undergraduate population should—other things being equal—see an

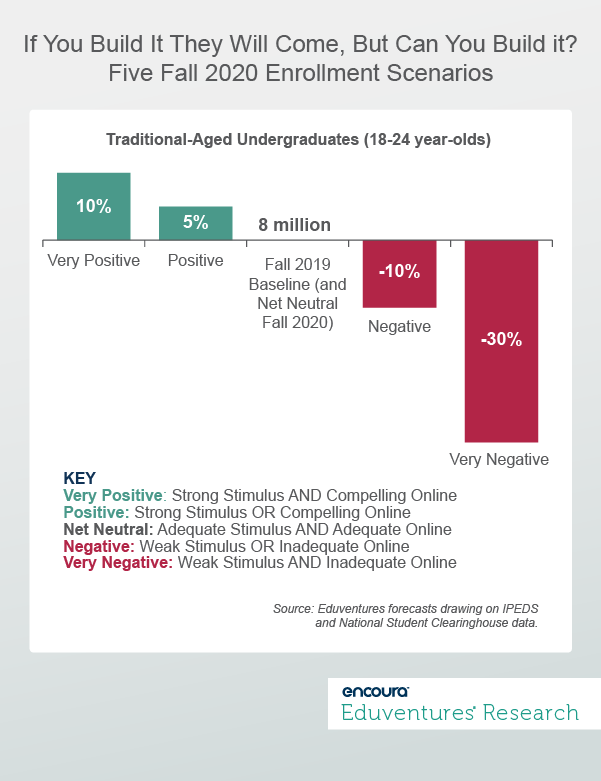

Figure 1 forecasts traditional-aged undergraduate enrollment for fall 2020 under different scenarios, compared to fall 2019.

Starting with the left side of the chart: why might enrollment grow?

The Positive Scenarios

As noted, most traditional-aged undergraduates, prospective and current, would prefer to enroll or re-enroll this fall as planned. If an ongoing health crisis curtails alternatives such as employment and travel, doing “nothing” at home for a semester or more looks unappealing, not least to their parents.

If federal stimulus, subsidizing either schools or families or both, is strong enough to match the scale of the downturn, many households will regard school as welcome continuity and an investment in the future. Since many jobs open to high school graduates will be unavailable mid-pandemic, a strong stimulus will persuade more young people than normal to enroll.

If schools can reimagine the traditional undergraduate experience online—going beyond the standard online playbook aimed at no-frills adults to encompass cohort bonding and extra-curriculars—then fall 2020 might be (almost positively) positioned as a creative hybrid of community solidarity and educational futurism. When other funding sources, notably states, the stock market, and philanthropy, are in doubt, schools need an online vision and reality that justifies standard tuition and funds financial aid.

This might prove to be a heavy lift: not simply to transition from emergency remote instruction to good online learning practice but to re-think, in a few short months, a modality that up to now most young people and many faculty members have dismissed out-of-hand. Striving for equitable access to any reimagined online model, when device and Internet provision are uneven, only adds to the challenge.

But progress, first and foremost, might not be a matter of fancy technology. Changing the narrative from “online is dull, isolating, and not what I paid for” to “online can be social, engaging, and fun” might be as much new mindset as new technology. A lull in the virus and herd immunity might permit colleges to offer some in-person experiences, but logistics will be tortuous.

If we can’t have college…

The Negative Scenarios

Turning to the right side of the chart: if the stimulus is found wanting, sickness and anxiety persist, and fall online learning comes across as transactional—more about schools shoring up their books than an engaging student experience—many students and families will defer or look elsewhere.

In almost any scenario, students will be more likely to study closer to home and at less expensive schools, favoring in-state publics and community colleges. The weaker the stimulus and more unappetizing the delivery mode, the more these schools stand to benefit. Fully online institutions may also do well. If family finances are really strained, low-priced online course providers, like Straighterline and Outlier, may rise in prominence with students and parents calculating that banking some general education credits may be the best way to ride out the crisis and get a jump on fall 2021. An austerity-driven DIY mentality may take hold, boosting the appeal of noncredit, self-paced MOOC-type courses. Some firms have made their course catalogs available free for a limited time.

The reason we are forecasting no more than a 10% enrollment year-over-year bump, sizeable by any conventional yardstick, but up to a 30% drop, is that college participation is already very high among this age group, meaning there is less room for growth.

Of course, the fall may see all five of these enrollment scenarios, and more, in play. The paths of individual schools will diverge, and some states may prove more adept than others at higher education crisis management. Wild cards include any federal decision to temporarily admit unaccredited providers to federal financial aid—the logic being that funding for short, low-priced, employer-facing programs is just what the economy needs. That may be true, but for 18-year-olds it will also blunt the short-term appeal of anything perceived, rightly or wrongly, as an expensive, low quality online degree program.

Another wild card would be federal or state public works programs, giving young people a productive alternative to college at a time of national need: such as helping to staff healthcare facilities or rebuilding the local economy.

The Bottom Line

While the next few months continue to be fraught with unknowns, a sober assessment of past trends and current variables, customized to local circumstances, will serve schools well. There are many things beyond the control of institutional leaders, including the spread of the virus, the public health response, and government stimulus. Therefore, it is best to focus where schools have real agency: the student experience and communicating it to current and prospective students, even as the traditional rhythms of recruitment are suspended.

If, come the fall, unemployment is still sky-high, state tax receipts are cratering, stock market returns are disappointing, and donors are holding back, the number one priority for schools is to ensure that the case for enrollment is rock solid.

Never

Miss Your

Wake-Up Call

Learn more about our team of expert research analysts here.

Eduventures Chief Research Officer at Encoura

Contact

Join us in Boston, November 1–3, 2020, as we convene eminent thinkers, leaders, and practitioners from across the higher education spectrum to examine and showcase the best ideas, old and new. If there is one event in higher ed you attend in 2020, make it Eduventures Summit.

Thursday, February 20, 2020 at 2PM ET/1PM CT

Research on your admitted students can provide enrollment leaders insight into why students enrolled in their institution -- and perhaps more importantly, why they didn’t -- but without benchmarks, an institution can only understand its result in isolation.

Inevitably, an institution is compelled to ask: How does its admitted student metrics look in comparison to other institutions in its category. Using data from the Survey of Admitted Students™, our latest benchmark report outlines the nine key benchmarks that every college and university can use to inform recruitment, yield, and institutional identity.

In this webinar, Eduventures Principal Analyst Kim Reid will identify key strategic questions every enrollment leader should be asking to measure up the institution’s yield performance and how to take specific action to improve your class.